Direct lending, which has topped South Korean institutional investors’ private debt strategies for years, has become even more popular amid rising interest rates, a survey found. More Korean investors are eyeing distressed debt and special situation strategy, targeting corporates in poor financial conditions this year.

The Korea Economic Daily conducted the survey of Korea’s 22 major institutional investors, including pension funds, mutual aid associations and insurers, early this year. Together they manage 2.11 quadrillion won ($1.59 trillion) in assets. Of the 22 investors, 20 manage 411.4 trillion won ($308.9 billion) in alternative assets.

(Graphics by Sunny Park)

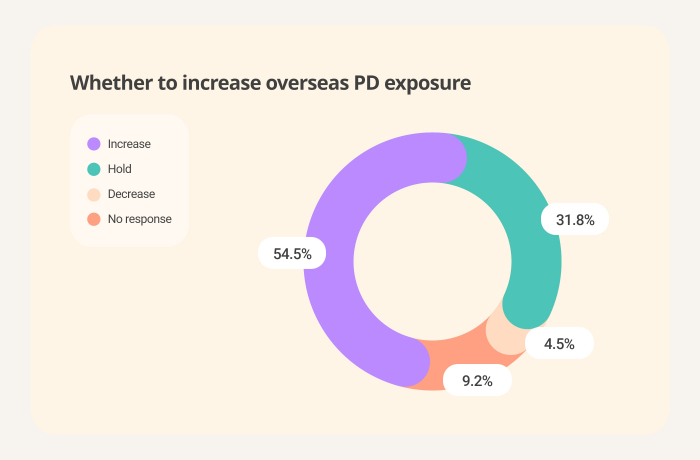

Some 55% of the investors will increase exposure to private debt in 2023, the survey found. About 32% will hold the current proportion, while 4.5% plan to cut the exposure.

Private debt was chosen as Korean institutional investors’ favorite asset class this year. In multiple choice questions, 16 investors said they will increase exposure to private debt. Infrastructure followed winning 12 votes; private equity and real estate were less popular with eight and two votes, respectively.

Private debt was the one that Korean investors felt was the most reasonably priced of the four alternative asset classes. Some 59% said private debt is fairly valued, and 18.2% thought it is moderately undervalued. About 14% said it is moderately overvalued; none of them stated it is highly overvalued.

Stable income topped the reasons for private debt investment. In multiple choice questions allowing up to two options, steady cash flow won 17 votes on the investment goal. Diversification and fixed income substitute received three and two votes, respectively.

(Graphics by Sunny Park)

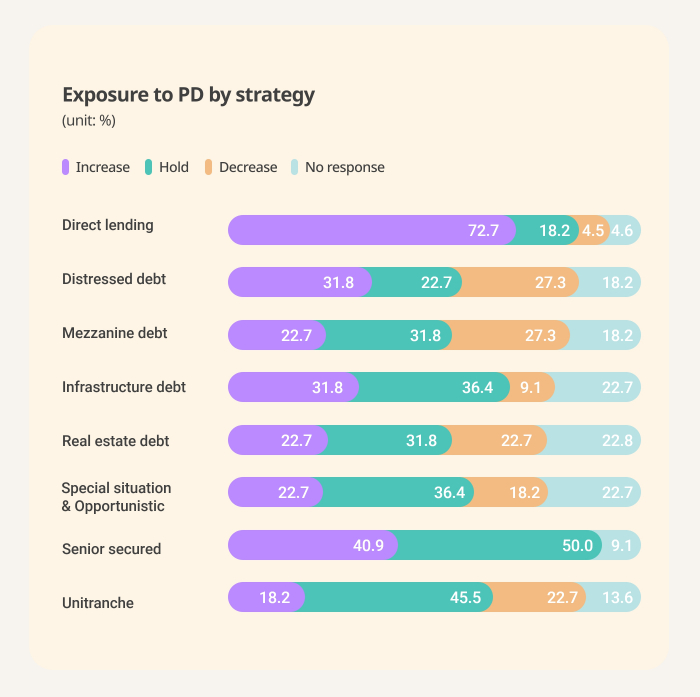

Direct lending, which was the preferred strategy for Korean debt investors in 2017, 2020 and 2022, has become further popular amid inflationary pressure and global rate hikes. Some 73% will raise the exposure to direct lending this year, compared with 61.5% last year, the survey found.

More Korean limited partners (LPs) are eyeing distressed debt and special situation & opportunistic strategy this year, targeting companies that are suffering financial difficulties and aiming for recovery. Some 32% of the surveyees said they will increase distressed debt, nearly double 15.4% a year ago. About 23% stated they plan to intensify special situation & opportunistic strategy, almost triple 15.4% in 2022.

But it is unclear that the investors will execute the strategies for distressed corporates, a source from an insurer that took the survey said.

“In the past, more investors used the strategies and made profits in short term. Today, there is less certainty on how long the current policies on interest rates and market conditions will last,” he said.

“It would be best if the valuations of the distressed companies had V-shaped rebound soon, but most investors are not sure this will happen in the near term,” the source added.

Infrastructure debt and real estate debt, which normally provide lower yields than direct lending, became less popular with Korean institutional investors. Some 32% said they will increase infrastructure debt, down from 50% last year. About 23% plan to raise exposure to real estate debt this year, compared with 38.5% in 2022.

Senior secured debt was chosen by 40.9% of the investors, similar to 42.3% last year. Half of the investors will maintain their current exposure to the strategy, up from 38.5% a year ago.

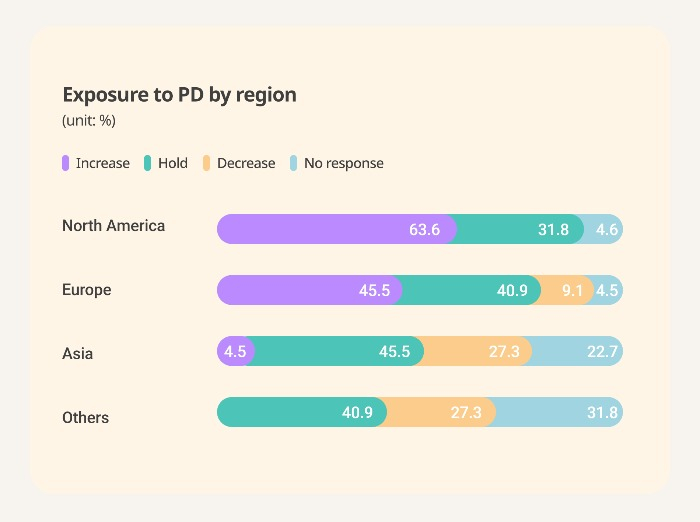

(Graphics by Sunny Park)

By geographical location, North America continued to be the top destination for Korean private debt investors. Some 64% will increase the asset class in North America, up from 50% a year ago. About 32% will hold the current proportion, and none of them will reduce assets from the region, the survey found.

The investors’ preference for European private debt remained similar to last year. Some 46% will raise exposure to the asset class in Europe, almost the same as 42.3% a year ago.

More Korean LPs are planning to decrease exposure to private debt in Asia. About 27% will reduce it, while 15.4% said they would do so last year. None of the surveyees stated they will increase Asian private debt; 45.5% will maintain the current proportion.

To view responses of individual institutions on their alternative asset allocation and fund manager selection, please visit Asset Owners Report.

Participants in this survey are as follows:

Public pensions and SWF

National Pension Service Korea Investment Corporation Government Employees Pension Service Teachers' Pension Korea Post (Insurance)

Mutual aids & associations

Yellow Umbrella Mutual Aid Fund Military Mutual Aid Association Public Officials Benefit Association Korean Federation of Community Credit Cooperatives The Korean Teachers' Credit Union

Insurers

Kyobo Life Insurance Samsung Life Insurance NongHyup Life Insurance NongHyup Property and Casualty Insurance Meritz Fire & Marine Insurance Samsung Fire & Marine Insurance Shinhan Life Insurance Hanwha Life Insurance Hyundai Marine and Fire Insurance ABL Life Insurance KB Insurance KB Life Insurance

Write to Jihyun Kim at snowy@hankyung.com Jennifer Nicholson-Breen edited this article.

We use cookies to provide the best user experience. By continuing to browse this website, you will be considered to accept cookies. Please review our Privacy Policy to learn our cookie policy.

Asset Owners ReportS.Korean LPs to up exposure to private debt, infrastructure in 2023: Survey

Asset Owners ReportS.Korean LPs to up exposure to private debt, infrastructure in 2023: Survey Private equityMore Korean LPs look to buyouts, special situations for private equity

Private equityMore Korean LPs look to buyouts, special situations for private equity Korean InvestorsS.Korean LPs name 41 best alternative asset managers

Korean InvestorsS.Korean LPs name 41 best alternative asset managers