SK Ecoplant seeks to absorb SK Materials' industrial gas units

SK Inc. plans to list SK Ecoplant after the merger

By Jun 24, 2024 (Gmt+09:00)

Samsung steps up AR race with advanced microdisplay for smart glasses

When in S. Korea, it’s a ritual: Foreigners make stops at CU, GS25, 7-Eleven

Maybe Happy Ending: A robot love story that rewrote Broadway playbook

NPS yet to schedule external manager selection; PE firms’ fundraising woes deepen

US auto parts tariffs take effect; Korea avoids heavy hit

SK Ecoplant Co., a South Korean construction engineering and waste management company, is seeking to absorb the profit-making subsidiaries of SK Materials Co., an industrial gas business unit within SK Inc, according to people with knowledge of the matter on Sunday.

The proposed merger, estimated to be in the billion-dollar range, is aimed at shoring up SK Ecoplant, a debt-laden company that had spearheaded mergers and acquisitions under the group’s “Deep Change” initiative over the past few years. Those M&As have yet to create synergy.

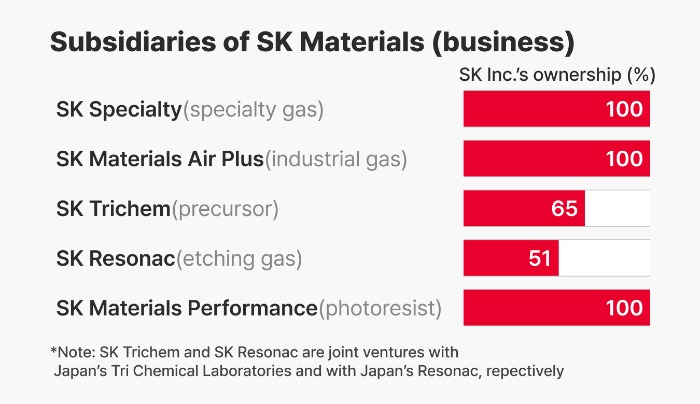

SK Materials’ subsidiaries that SK Ecoplant is considering taking over include SK Materials Airplus Inc., SK Materials Performance Co. and SK Trichem Co. SK Trichem is a joint venture with Japan’s Tri Chemical Laboratories and SK Inc., which holds a 65% stake in the venture.

They provide industrial gases such as liquefied oxygen, nitrogen and argon used at SK's affiliated companies such as SK Hynix Inc. and SK Energy Co., a petrochemical company, under long-term contracts, thus earning steady profits.

Their consolidated operating profit reached 213.0 billion won ($153 million) in 2023 on sales of 1.21 trillion won.

The proposed deal will exclude SK Specialty, according to the sources.

SK Group will confirm the combination of SK Materials' industrial gas units and SK Ecoplant as early as July, the sources said.

SK Group had previously considered selling all subsidiaries of SK Materials and pumping the proceeds into SK Ecoplant. But it has switched into a plan to combine SK Materials’ units, excluding SK Specialty with SK Ecoplant, although they have no overlapping businesses.

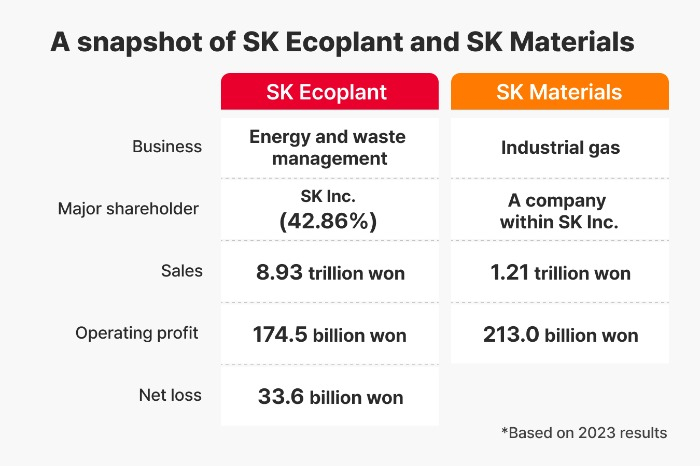

In 2023, SK Ecoplant logged a net loss of 33.6 billion won though it earned 174.5 billion won in operating profit.

Its short-term debts coming due within the year nearly tripled to 1.67 trillion won as of the end of March this year, compared with 596.3 billion won as of the end of 2021.

Since 2020, SK Ecoplant has poured more than 4 trillion won in eight acquisition deals, including the purchase of EMC Holdings, to pivot toward the waste management business, beyond construction engineering.

The mooted merger is part of ongoing restructuring at the country’s No. 2 conglomerate, which includes a possible combination between SK Innovation Co. with SK E&S Co., a liquefied natural gas (LNG) supplier.

SK Innovation is the parent of South Korea’s largest oil refiner SK Energy Co. and battery maker SK On Co.

The business group has financed M&As mostly with loans that raised its debt-to-equity ratio to as high as 400% at one point. Its plan to raise money from an IPO went awry amid high interest rates.

It has then shifted to private equity funds for financing, for which it now needs to pick up the bill.

With little signs of a turnaround in its rechargeable battery and waste management units, the group's core businesses alongside biotech and semiconductor, industry observers said the cumulative losses at battery maker SK On and SK Ecoplant will take a heavy toll on SK Group.

SK Group is sticking to its plan to list SK Ecoplant after absorbing SK Materials' money-making industrial gas subsidiaries.

In return for transferring SK Materials' units to SK Ecoplant, SK Inc. will receive newly issued shares of Ecoplant. SK Ecoplant’s enterprise value is estimated at 5 trillion won, down from over 8 trillion won last year.

SHAREHOLDER APPROVAL

Hurdles remain. They need to win approval from SK Ecoplant's major shareholders, including eight investment companies such as Brain Asset Management Co., IUM Private Equity and Korea Investment & Securities Co. to move forward with the merger between SK Ecoplant and the industrial gas units.

The investment firms could urge the construction engineering company to focus on turning around before absorbing SK Materials’ subsidiaries.

For SK Inc., it needs to persuade its shareholders to approve taking over SK Ecoplant’s shares in return for transferring SK Materials’ cash cows to the former.

“The key will be how much SK Ecoplant’s shares will be valued in the merger process,” said a stock market analyst.

Asked about the possible merger between SK Ecoplant and SK Materials’ units, SK Group said it is looking into various measures but that nothing has yet been determined.

KKR

Meanwhile, to proceed with the merger between SK Innovation and SK E&S, the latter may need to pay some 3.14 trillion won to KKR & Co. to buy back that amount of shares it had issued to the private equity firm between 2021 and 2023, said investment bankers.

The redeemable convertible preferred shares sold to KKR are collateralized by SK E&S’ seven fully owned industrial gas-related companies.

Write to Jun-ho Cha and Ji-Eun Ha at chacha@hankyung.com

Yeonhee Kim edited this article.

-

Corporate restructuringSK asks KDB for further funding before drastic restructuring

Corporate restructuringSK asks KDB for further funding before drastic restructuringJun 20, 2024 (Gmt+09:00)

3 Min read -

Mergers & AcquisitionsSK Innovation looks to merge with SK E&S for organic growth

Mergers & AcquisitionsSK Innovation looks to merge with SK E&S for organic growthJun 20, 2024 (Gmt+09:00)

3 Min read -

Corporate strategySK's Chey rebuts court's SK unit value estimate for divorce

Corporate strategySK's Chey rebuts court's SK unit value estimate for divorceJun 17, 2024 (Gmt+09:00)

3 Min read -

Corporate restructuringSK embarks on business overhaul to focus on mainstays

Corporate restructuringSK embarks on business overhaul to focus on mainstaysMay 29, 2024 (Gmt+09:00)

4 Min read -

Corporate strategySK Group to pursue employee-led ‘deep change’

Corporate strategySK Group to pursue employee-led ‘deep change’Aug 21, 2023 (Gmt+09:00)

2 Min read -

Corporate strategySK Group reworks 'financial story' action plans

Corporate strategySK Group reworks 'financial story' action plansAug 26, 2022 (Gmt+09:00)

2 Min read -

Behind the ScenesSK Group’s 'financial story' running out of steam?

Behind the ScenesSK Group’s 'financial story' running out of steam?Jun 14, 2022 (Gmt+09:00)

5 Min read -

SK Group's financial story: Measure, divest and focus

SK Group's financial story: Measure, divest and focusMar 09, 2021 (Gmt+09:00)

5 Min read -

Private equitySK Group's PE-funded transformation in the spotlight

Private equitySK Group's PE-funded transformation in the spotlightMar 07, 2022 (Gmt+09:00)

5 Min read -

-

Mergers & AcquisitionsSK Ecoplant buys e-waste recycling firm for $1 bn

Mergers & AcquisitionsSK Ecoplant buys e-waste recycling firm for $1 bnFeb 21, 2022 (Gmt+09:00)

2 Min read -

Corporate restructuringSK's 5-year journey toward batteries, bio and chips

Corporate restructuringSK's 5-year journey toward batteries, bio and chipsJan 23, 2022 (Gmt+09:00)

3 Min read